Previous Story

Ceilings at interest rates impacted on microcredit in Ecuador

Posted On 04 Jun 2019

Ecuadornews:

Since 2009, the Government has set the maximum interest rates that private banks can charge for lending money to their clients. But these rules could change.

The delegate of the Executive before the Board of Monetary and Financial Policy and Regulation, Marcos Lopez, announced last week that the Government will begin to review these regulations from the second half of this year.

A first step will be to review the formula for calculating the ceilings of the rates, and in 2020 the costs of lending money in certain loan segments would be analyzed, with the preparation of a technical study, López said.

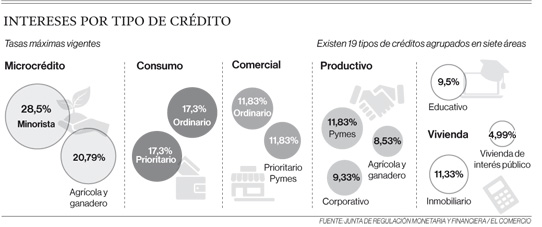

Currently, for each of the 19 types of credits there is a maximum interest rate. Banks can not exceed these limits, which vary according to the segment.

For example, the productive credit requested by companies has a ceiling of 10.21%; while consumer credit, which is usually granted for the purchase of vehicles, reaches 17.3%. A microcredit, that is, a loan for a small business, has a maximum rate of 28.5%.

One of the studies that has measured the impact of policies in the financial sector in the last nine years was carried out by the Network of Financial Institutions of Development (RFD) in 2018. According to that report, called ‘Incidence of changes in public policy ‘, the amounts of microcredit granted by the private financial system in the country grew between 2008 and 2017, but the number of operations fell.

The latter went from around 1.2 million in 2008 to around 900,000 in 2017. One of the explanations is that financial institutions may have opted to deliver higher amounts of credit to cover the decrease in income from limits to interest rates.

This reflects, according to Julio José Prado, president of the Association of Private Banks (Asobanca), that the policy of rate ceilings has deteriorated the levels of access to credit for microbusinesses, small and medium enterprises.

“There are interest rates that do not compensate for the risk of granting credit, such as microcredit and the loan granted to SMEs. As the risk of the operation is not covered, the result is that many people are unable to access a formal loan. ” A possible liberalization of interest rates generates expectations in the sector, since it would make it possible for banks to charge for each loan according to the client’s credit history and in accordance with the placement cost generated by the bank to carry out the operation.

For example, if you are dealing with a client with a good payment history, you would be offered a lower rate than a person who has incurred in arrears or who has never asked for a loan before.

This last client would not be denied financing, but would have to pay more, explained the president of Asobanca. The Delegate of the President to the Board explains that these issues have to be discussed so that interest rates are related to the market.

He explained that currently the formula to set interest rates are not technical, but they depend even on the decision of the current government. The spokesperson of the Asobanca adds that since the Central Bank of Ecuador (ECB) began to fix ceilings the entities never knew what is the formula used by the entity.

Sonia Zurita, teacher of the Espace, Espol Business School, says that the release of roofs can not be understood as a rise or a drop in rates, because if there is more credit available and banks fight to attract customers, the rates may tend to fall.

But it will also depend on the liquidity in the economy. In 2017, when the country registered excess liquidity, the benchmark interest rates; that is, the average rates charged by banks were below the ceilings. In the last eight months, in view of lower deposit growth, reference rates are closer to the ceilings.

In May 2017, the reference rate for corporate productive credit was 7.61% and in May of this year, the reference rate for that same credit was 9.25%. According to an analysis by Alfredo Vergara, former Superintendent of Banks, from 2007 to 2009, when there were no limits to the collection of interest, the rates fell 15% on average, but after the regulation the reduction ranged between 1% and 2%, on average .

He believes that if the ceilings are released and also the exit tax on foreign currency (ISD) is eliminated, the country will be more attractive for more capital and new banks to arrive. With this he says it is to be expected that the interest rate will be lower. (I)

Source: https://www.elcomercio.com/actualidad/techos-tasas-impacto-microcredito-bancos.html